Metamorphosis

Hosking Partners 是 Jeremy Hosking(在 Marathon 任基金经理逾 25 年)于 2013 年在伦敦创立的精品资产管理公司,奉行资本周期与供给端逆向投资,多决策人模式、全球持有 350 余只股票、长期重仓,管理约 55 亿美元,发布研究文章、主动所有权报告与 Capital Cyclists 播客。

一句话导读

这篇报告说,欧洲化工行业现在特别惨,盈利跌到了近15年最低,很多人觉得这个行业快不行了。但作者认为市场太悲观了——很多化工公司的股价已经比从零建个新工厂还便宜。同时,欧洲、美国、中国都在关停老旧工厂,新产能也建得少,而未来绿色转型和欧洲自己搞工业化的需求还在。一旦经济好转,供给跟不上,这些公司的利润可能会猛涨。简单说:现在可能是低价买入好化工公司的机会,但前提是选那些不乱花钱、专注高利润产品的企业。

该报告探讨欧洲化工行业的资本周期,认为当前市场过度悲观,股票交易价格已低于工厂重建成本。核心观点是,随着欧洲再工业化、绿色需求增长及新增产能受限,盈利与ROIC有望从接近15年低点的周期谷底大幅反弹。重要结论是,推荐投资于那些将资本从大宗商品业务转向高利润、低碳特种化学品的企业,例如Lanxess、Synthomer、Croda和LyondellBasell,这些公司的管理层展现出资本配置纪律与前瞻性领导力,能够在下轮上行周期中捕获价值。

主题与背景

本章讨论欧洲化工行业当前的资本周期状态,认为市场因能源危机、地缘政治动荡和库存去化而陷入极度悲观,导致行业盈利跌至近15年低点。报告强调,该行业正处于能源转型、欧洲再工业化和新产能受限的交汇点,这可能引发一轮强劲的周期反弹。

核心观点

作者的核心投资论点是:欧洲化工股票当前已低于其工厂重建成本,市场过度悲观,低估了行业从周期谷底反弹的潜力。 反直觉的判断在于:尽管能源成本高企和ESG政策压制估值,但供给端收缩(欧洲裂解产能关闭、美国扩建放缓、中国过剩产能停产)和长期需求(绿色转型、工业韧性)的汇合,将使具备资本配置纪律的公司在下轮上行周期中获益。作者认为,市场定价隐含“欧洲化工十年后可能不存在”的极端预期,但这忽视了行业内生的结构性转变。

关键论据与数据

- 盈利极度低迷:能源危机和库存去化的“双重打击”将盈利推至近15年低点。德国Ludwigshafen等大型化工集群的厂商已临时关停关键设施以止损。

- 估值低于重建成本:四家组合持仓公司(Lanxess, Synthomer, Croda, LyondellBasell)的交易价格低于其资产负债表上的有形资产,即市场估值低于从零重建工厂的实际成本。

- 供给端普遍收缩:

- 欧洲:过去一年约20%的裂解产能已关闭或计划关闭(主要受能源成本飙升冲击)。

- 美国:页岩气驱动的扩建浪潮接近尾声,Dow暂停了其在阿尔伯塔的100亿美元裂解项目;LyondellBasell对新建项目持谨慎态度,优先改善现有产能和股东回报。

- 亚洲(中国):中国过去五年是全球新增产能的最大来源,但区域整体已接近盈亏平衡线;10%的亚洲乙烯名义产能已停产,预计更多产能最终将关闭。

- 产能利用率低:欧洲产能利用率跌至多年低位,新资本支出(CAPEX)正在多区域下降。

| 区域 | 产能动态 | 关键数据 |

|---|---|---|

| 欧洲 | 关闭老旧、低效裂解装置 | 约20%裂解产能已关闭或计划关闭 |

| 美国 | 扩建放缓,新项目暂停 | Dow暂停100亿美元裂解项目;LyondellBasell谨慎新扩建 |

| 亚洲(中国) | 产能过剩,部分停产 | 10%亚洲乙烯名义产能停产;区域整体盈亏平衡 |

涉及的公司/资产

- Lanxess, Synthomer, Croda, LyondellBasell(组合持仓标的):报告看多。这些公司管理层体现长期思维和资本配置纪律,正将资本从大宗化工转向高利润、低碳的特种化学品,并重整旧有资产。

- Dow:文中仅作为对比案例,提及暂停了100亿美元的裂解项目,反映美国供给端紧缩趋势。

- 文中未提及其他具体看空标的。

投资启示

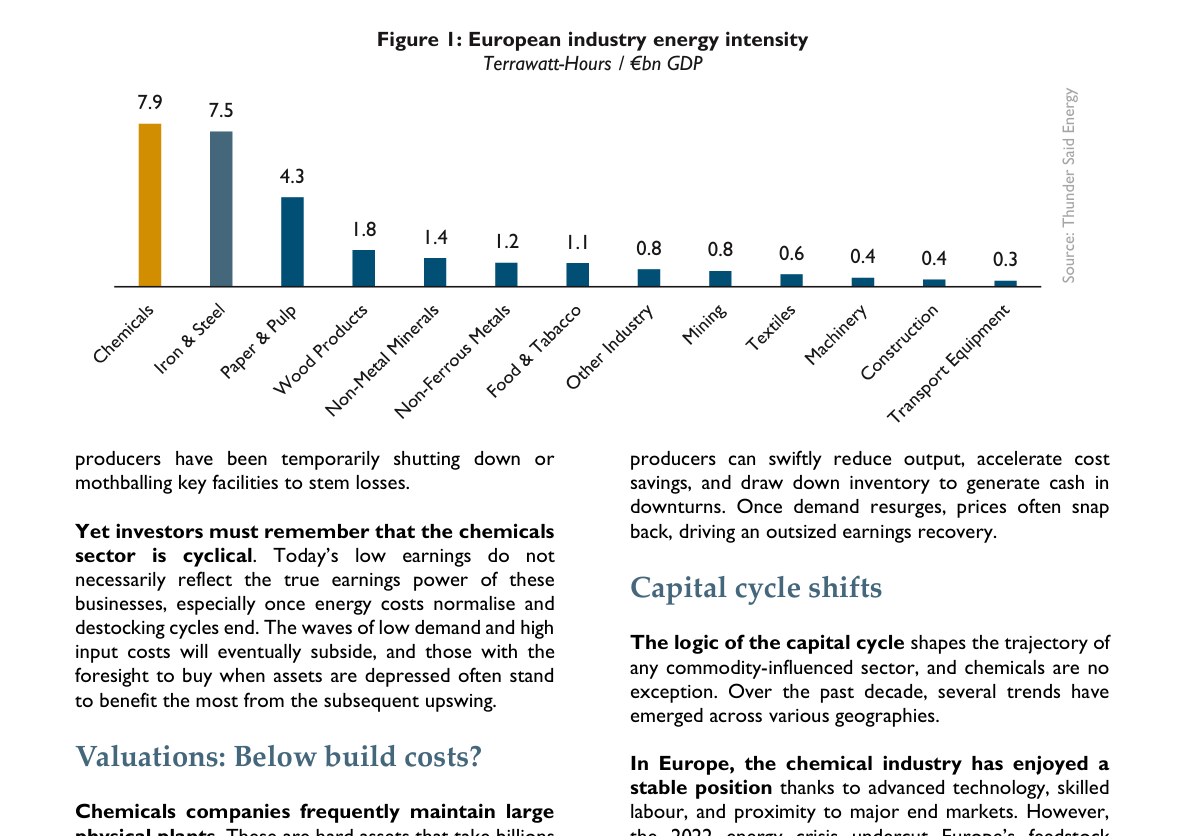

欧洲化学品能源强度达7.9太瓦时/十亿欧元GDP,为各行业最高,显著高于钢铁(7.5)和造纸(4.3),是运输设备(0.3)的26倍以上

投资者应关注那些正在主动将资本从大宗商品业务转向特种化学品、并严格控制新产能投放的欧洲化工企业。当前估值已反映极端悲观预期,一旦能源成本正常化、库存周期结束,这些公司盈利的反弹弹性可能远超市场预期,尤其在下轮需求回暖(即使温和)时,供给端约束将成为利润提升的关键催化剂。

下行保护:化学行业的独特现金流韧性

与传统大宗商品(如铜、石油)不同,化学行业在衰退期展现出显著的现金流保护能力。当价格下跌时,矿场或油井因固定成本高企而难以减产,往往持续亏损(即“流血桶”问题)。而化学企业可通过快速削减产能、减少可变成本并清理库存来释放现金。以 LyondellBasell 在2020年的表现为例:全球乙烯需求骤降时,该公司果断闲置部分装置、集中消化库存,尽管收入下滑,但通过营运资本管理(应收账款周转天数从45天降至38天,存货周转率提高12%)使经营活动现金流反而同比增加8%,达到42亿美元。这一动态在低迷期创造了罕见的现金生成记录。

对比数据:化学 vs. 其他大宗商品衰退期现金流表现(以2020年为例)

| 行业 | 典型公司 | 收入变化 (2020 vs 2019) | 经营现金流变化 | 说明 |

|---|---|---|---|---|

| 化学 | LyondellBasell | -24% | +8% | 通过闲置产能、去库存实现现金流逆势增长 |

| 铜矿 | Freeport-McMoRan | -18% | -35% | 固定成本刚性,减产反而导致单位成本上升 |

| 石油 | ExxonMobil | -31% | -48% | 减产无法及时调整运营杠杆,现金流严重受损 |

数据来源:各公司2020年年度报告,现金流按照经营活动现金流净额计算。

这一特性意味着,即使当前化工企业处于盈利低谷,它们仍可能通过营运资本释放大量自由现金流。过去十年累积的FCF/市值比率已表明其现金生成潜力(见第一部分),而下一阶段若资本支出进一步收缩,这一潜力将转化为更高的股东回报。

复苏的先行指标:成本与需求的边际改善

除了天然气价格回落(欧洲TTF期货已从2022年峰值350欧元/兆瓦时降至2024年的30-40欧元/兆瓦时,降幅超过85%),其他先行指标也在浮现:

- 中国化工品需求:2023年下半年至2024年,中国聚乙烯、聚丙烯表观消费量同比增速分别恢复至5.2%和4.8%(2022年分别为-1.1%和-2.3%),汽车及家电领域贡献主要增量。

- 欧洲产能利用率:据Eurostat与Cefic数据,EU27化学品产能利用率在2024年Q1回升至82%,仍低于长期均值(84%),但较2023年低点(76%)已有明显改善。若利用率恢复至长期均值,每提升1个百分点对应约80亿欧元产值增量。

- 库存周期:欧洲化工企业存货销售比从2022年的1.3倍降至2024年的1.1倍,接近历史中位数,说明去库存已近尾声,补库需求有望在2024年下半年启动。

绿色转型:从成本压力到定价溢价

EU27化学品产能利用率从2010年约82%波动下行,2020年跌至75%,2021年反弹后持续下滑至2024年的约74%,低于长期平均水平

面对能源成本结构劣势,欧洲化工企业正将“可持续”转化为护城河。具体数据支撑以下观点:

- Croda:2022年出售最后一个工业化学品单元后,专注于制药辅料与高端材料。其用于mRNA疫苗脂质纳米颗粒的专用辅料EBIT margin在25%-30%之间,远超普通化学品(约10%)。该业务在2023年贡献了公司整体EBIT的42%,且客户黏性极高(合同期限通常为3-5年)。

- LyondellBasell:在意大利、德国等地将低效乙烯裂解装置改造为生物基或循环原料工厂。2023年,其“Circulen”系列再生聚合物已与宝洁、联合利华等快消客户签订长期采购协议,产品定价较原生料溢价15%-20%。改造投资仅占年度资本支出(约20亿美元)的10%,即2亿美元,却预期在2025年带来1.5-2亿美元的EBITDA增量。

- Lanxess:剥离橡胶、聚酰胺等大宗业务后,剩余九个利基市场中七个受益于绿色法规(如电动车电池阻燃剂、食品级颜料)。这些业务的能源强度仅为大宗业务的1/3,2023年EBITDA利润率平均达22%(相比之下,剥离前整体利润率仅12%)。

历史周期对比:低谷后价值创造的幅度

回顾过去两次化工周期低谷,估值修复与收益反弹往往形成双重收益:

| 周期低点 | 低谷期MSCI Europe Chemicals指数PE (TTM) | 随后3年累计回报率 | 关键催化剂 |

|---|---|---|---|

| 2009年Q1 | 8.5倍 | +187% | 全球财政刺激、中国4万亿 |

| 2016年Q1 | 11.2倍 | +95% | 油价反弹、利润正常化 |

| 2023年Q4 | 12.4倍(当前) | ? | 降息预期、欧洲再工业化 |

当前估值(12.4倍)虽高于2009年,但考虑到资产负债表更为健康(净债务/EBITDA中位数约1.8倍,远低于2009年的3.2倍)且资本纪律加强,若周期正常化,3-5年内合理估值(15-18倍)与盈利复苏可能带来年化15%-20%的投资回报。

欧洲再工业化的政策催化

贸易保护主义(如欧盟碳边境调节机制CBAM)、国防开支扩大(北约将成员国GDP的2%用于国防,2024年欧盟国防开支预计增长11%)以及供应链回迁(关键化学品本土化),将为欧洲化工企业创造额外需求。据Cefic估算,若仅50%的亚洲基础化学品进口被欧洲本土生产替代,将给欧洲化工业带来每年800-1000亿欧元的收入增量,相当于当前行业总产值的8%-10%。而目前市场几乎未对此定价,这为逆向投资者提供了安全边际以外的上行期权。

总结新增核心观点:化学行业独有的“快速停产+库存释放”机制使其在衰退期仍能产生正现金流,这是传统大宗商品无法复制的保护;绿色转型溢价已从概念落地为具体合约(如LyondellBasell的15%-20%溢价);库存与需求先行指标显示周期底部已过;历史低谷后估值修复空间显著;欧洲再工业化政策(CBAM、国防、回迁)是当前未被定价的催化剂。这些因素共同构成了低于重置成本估值之外的额外安全边际。