Masters of the Air (March 2026)

The Capital Cycle 是伦敦资管公司 Marathon(1986 年由 Ostrer、Arah、Hosking 创立)于 2024 年推出的官方播客,由金融史学家 Edward Chancellor 主持,访谈其投研团队、讲解每期《全球投资评论》投资人信,秉持长期逆向的「资本周期」供给侧投资思想。

一句话导读

这篇报告讲的是欧洲航空航天业,核心观点是:现在飞机订单排到2030年后,新飞机交付要等5年,所以旧飞机飞得更久、修得更勤。最赚钱的不是造飞机的空客或波音,而是造发动机的公司(比如罗尔斯·罗伊斯、赛峰)。它们的商业模式像“剃刀-刀片”——卖发动机赚一次,后续维修保养持续收钱。供给越紧张,维修需求越大,利润弹性越高。对普通投资者来说,这意味着关注发动机OEM(原始设备制造商)可能比关注飞机制造商更有机会。

这篇报告探讨了欧洲航空航天业的历史与投资前景。核心观点是,由于供给端长期受限(行业寡头垄断、资本周期后的整合),发动机OEM(如Rolls-Royce、Safran、MTU)将迎来持续增长。重要结论:Rolls-Royce过去5年跑赢基准MSCI Europe达+995%,目前估值41x 2026e PE;Safran为30x,MTU更合理为24x。报告认为,空客与波音的寡头格局稳固,中国尚未成为可信竞争者,供给紧张为相关股票带来“蓝天”前景。

主题与背景

该章节回顾了欧洲航空航天业从20世纪初至今的发展史,并聚焦于其当前的投资前景。报告指出,欧洲在航空工业领域具备全球竞争力,其寡头垄断的市场结构(飞机制造双头垄断、发动机制造寡头垄断)是当前相关股票表现强劲的核心逻辑基础。

核心观点

作者的核心论点是:由于供给端极度紧张(波音/空客订单排到2030年代、宽体机交付等待时间翻倍至5年),以及行业资本周期后的整合,发动机OEM(Original Equipment Manufacturer)是最受益的环节。该判断逆市场共识之处在于:投资者通常关注飞机制造商(如空客)的需求,但作者认为发动机OEM的“剃刀-刀片”商业模式在供给短缺周期中更具盈利弹性。

关键论据与数据

飞机交付等待时间从2000年的约2年增至2025年的约5-6年,宽体客机等待时间最长

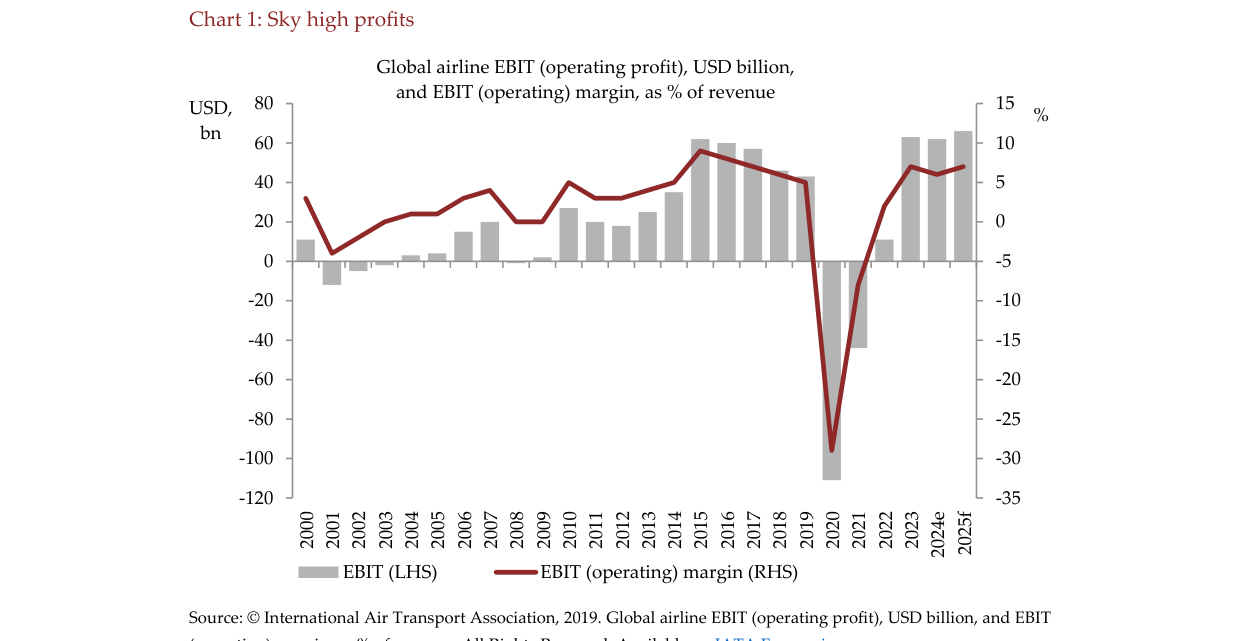

全球航空公司EBIT在2020年降至约-1000亿美元后强劲反弹,2025年预测达约700亿美元,EBIT利润率回升至约10%

1. 需求结构性增长:全球航空旅行需求自1990年以来年均增长+5%,且每次重大冲击后均反弹。新兴市场潜力巨大:

| 国家/地区 | 人均年飞行次数 |

|---|---|

| 美国 | 2.2次 |

| 欧洲 | 1.9次 |

| 中国 | 0.6次 |

| 巴西 | 0.5次 |

| 印度 | 0.1次 |

2. 供给端极度紧张:

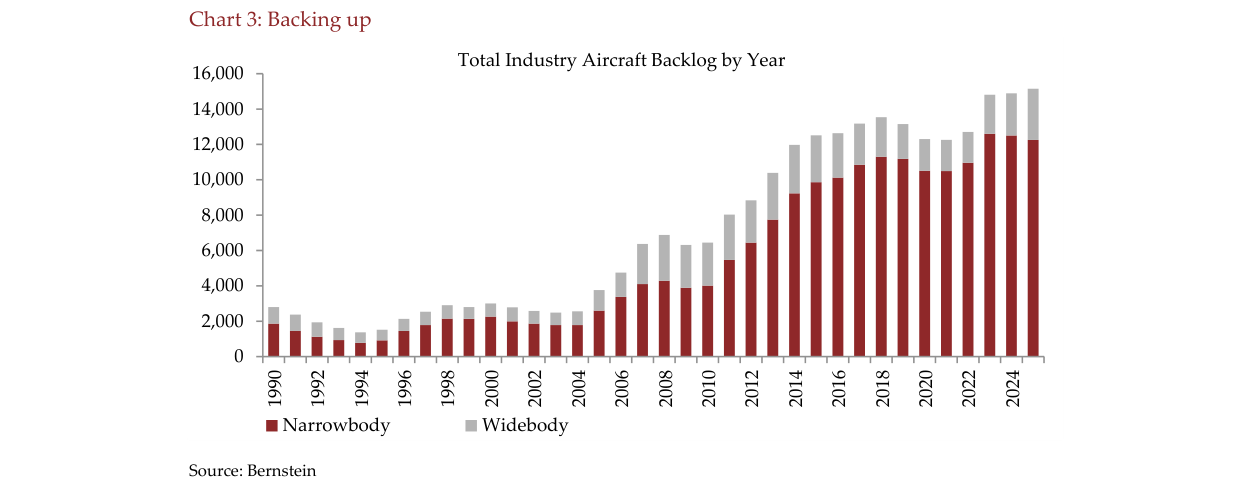

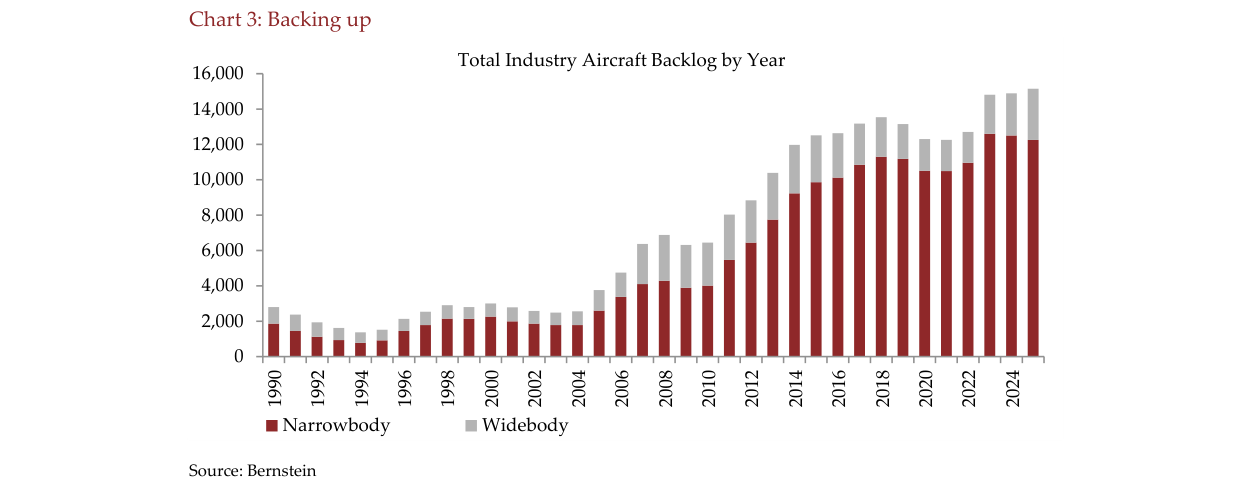

- 波音和空客订单积压达到创纪录水平(数据来源:Bernstein图表显示积压订单超过14,000架)。

- 宽体机交付等待时间从约2年翻倍至5年。

- 空客计划到2027年达到每月75架的生产目标,但市场共识基于其过往表现对其能否达成存疑。

3. 发动机OEM商业模式受益:

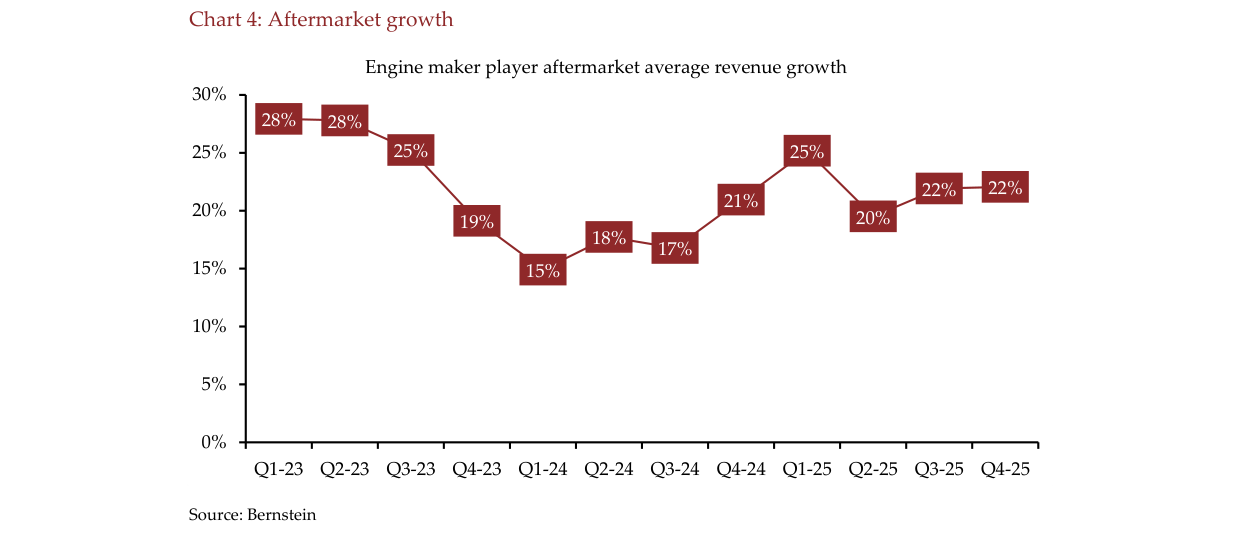

- 现有机队飞行时间延长,后市场服务(MRO)需求激增,推动发动机OEM的后市场收入增长(图表显示平均增长率在15%-28%之间)。

- 资产负债表改善,使公司有能力通过分红和回购超预期回报股东。

全球飞机订单积压量从1990年的约2500架持续增长至2024年的约15000架,窄体机占比约80%

涉及的公司/资产

- Rolls-Royce:看多。Marathon European团队的重仓股。在过去5年跑赢基准MSCI Europe达+995%(总回报+1153%)。当前估值为41x 2026e PE。CEO被视为成功执行了欧洲企业史上最成功的转型之一。

- Safran:看多。估值相对合理,为30x 2026e PE。受益于CFM56等发动机的后市场需求。

- MTU Aero Engines:看多。估值在三者中最为合理,为24x 2026e PE。

- GE Aerospace(美国):对比公司,估值同样为41x 2026e PE。

- Airbus / Boeing:供给侧受限的“瓶颈”方,其产能瓶颈为发动机OEM创造了有利条件。

- Alten:看空/表现不佳。Marathon组合中的小型持仓,因欧洲汽车客户受中国竞争和通胀冲击,表现低于预期。

发动机制造商售后市场收入增速从2023年Q1的28%波动下降至2024年Q3的17%,预计2025年Q4回升至22%

投资启示

1. 增持发动机OEM:核心策略是利用供给短缺的确定性机会。尽管预估估值较高(Rolls-Royce和Safran),但报告认为其未来数年EPS增速(中高两位数)能够消化当前估值。

2. 关注后市场服务:投资逻辑的核心是“旧飞机更需维护”,这为发动机制造商提供了稳定的、可预期的长期现金流(时间与材料合同、长期服务协议)。

3. 警惕供应链风险:报告间接提示,投资上游或下游的“一般供应商”(如Alten)可能面临汽车等其他行业拖累的风险,聚焦于发动机OEM的寡头地位是更确定的选择。