AI and the Material World (May 2026)

The Capital Cycle is the official podcast that Marathon Asset Management (the London firm founded in 1986) launched in 2024, hosted by financial historian Edward Chancellor, who interviews Marathon's investors about each Global Investment Review letter — applying the firm's long-term, contrarian "capital cycle" supply-side approach.

In plain words

This report warns that AI-related investments now make up over 40% of U.S. economic growth, while other sectors are shrinking. Meanwhile, emerging market stock indexes are heavily dominated by a few countries (like South Korea and Taiwan) and tech hardware, creating concentrated risk. The author argues AI stocks are overpriced and risky, and suggests looking instead at asset-heavy, cash-rich industries like energy, industrials, and telecoms. Worth reading because it offers a contrarian view against the AI hype.

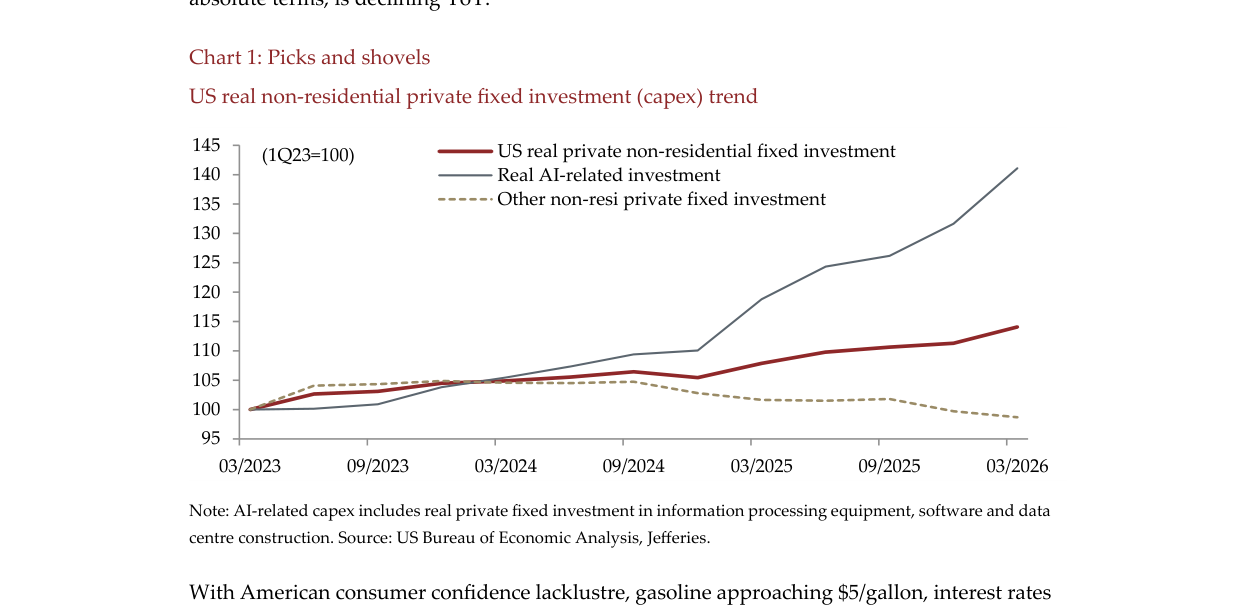

This report explores the capital cycle risks under the dominant AI theme. The core argument: AI-related capital expenditure now accounts for over 40% of U.S. GDP growth, while non-AI capital expenditure has declined in absolute terms year-over-year; weak U.S. consumer confidence, gasoline near $5 pe

Theme and Background

This chapter discusses the extreme capital cycle phenomenon driven by the AI theme. The report points out that AI-related capital expenditures have accounted for over 40% of US GDP growth, while non-AI capital expenditures have declined year-on-year in absolute terms. Meanwhile, weak US consumer confidence, gasoline prices near $5 per gallon, and sticky interest rates make the AI theme "too big to fail." Asset allocators are funneling large amounts of retirement capital through passive investing and private markets, further concentrating risk.

Core Thesis

The author's core investment argument is: the downside risk of the AI theme is more worth watching than the opportunity of continuing to overweight it. Counterintuitive judgments include:

- The AI theme has spread from US hyperscalers to the Asian supply chain, but stock prices far exceed fundamental support

- The MSCI Emerging Markets Index is dominated by South Korea, Taiwan, and semiconductor/tech hardware companies, lacking true diversification

- For companies deep in the supply chain, the main barriers are capital and time, not geological constraints, so the capital cycle is difficult to break

- The author believes opportunities lie in "everything else," not the AI theme

US real AI-related investment surges from a base of 100 in March 2023 to approximately 140 in March 2026, while other non-residential private fixed investment declines to about 98

Key Arguments and Data

1. AI capital expenditure dominates the US economy:

- AI-related capital expenditures account for over 40% of US GDP growth

- Non-AI capital expenditures are declining year-on-year in absolute terms (Chart 1 shows the trend)

- Weak US consumer confidence, gasoline prices near $5 per gallon, sticky interest rates

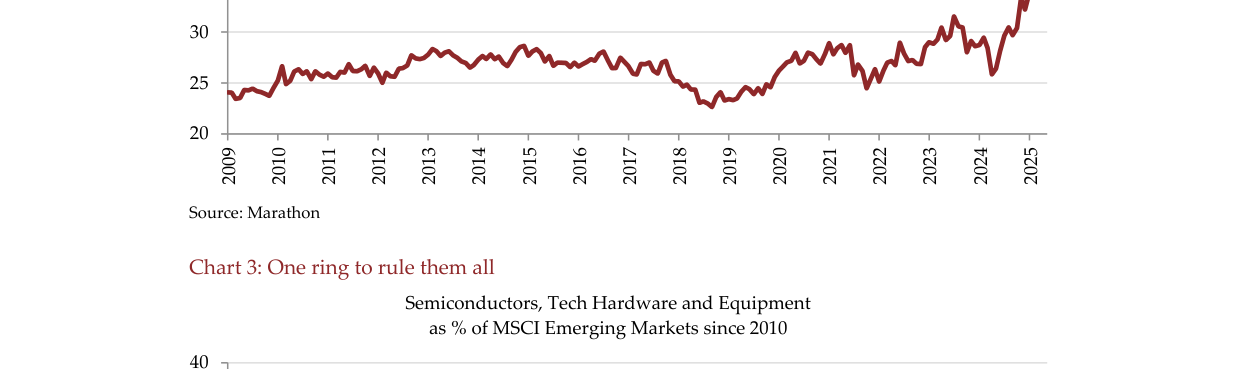

2. MSCI Emerging Markets Index concentration:

- The weight of South Korea and Taiwan in the MSCI Emerging Markets Index has been rising since 2010 (Chart 2)

- The weight of semiconductors and tech hardware in the MSCI Emerging Markets Index has been rising since 2010 (Chart 3)

The combined weight of South Korea and Taiwan in the MSCI Emerging Markets Index rises sharply from about 24% in 2009 to approximately 46% in 2025

3. Valuation and capital flows:

- Asian tech sector Price/Book valuations are at historical highs (Chart 4)

- The cost of capital for AI-themed companies has collapsed, while it has risen relatively for other sectors

- This "crowding out effect" will weaken the capital cycle in the tech sector while forcing rationalization of competition in other industries

4. Portfolio allocation:

- Asset-heavy industries (Chinese real estate, basic materials, industrials, energy, telecom) account for more than one-third of the EM portfolio

- High-yield financial businesses account for 25%

- More than half of the EM portfolio is outside Asia’s tech-heavy and competitive markets

The weight of semiconductors and tech hardware equipment in the MSCI Emerging Markets Index surges from about 11% in 2009 to approximately 38% in 2025

Companies/Assets Involved

| Company/Asset | Role | Key Data | Bullish/Bearish |

|---|---|---|---|

| TSMC | Core of Asian tech supply chain | Held for over a decade, largest position in EM portfolio | Bullish (excellent management), but stock price far exceeds fundamentals |

| Delta Electronics | Data center cooling equipment supplier | Bought during the COVID-19 pandemic | Bullish (excellent management), but stock price far exceeds fundamentals |

| Mediatek | Semiconductor design company | Bought during the COVID-19 pandemic | Bullish (excellent management), but stock price far exceeds fundamentals |

| OpenAI, Anthropic, SpaceX | AI-themed companies approaching IPO | May be rapidly included in global indices | Bearish (increases concentration risk) |

| Chinese internet companies | Branded consumer businesses | Long-term underweight | Bearish (structural barriers to entry declining) |

| Indian companies (multiple sectors) | Important index constituents | Long-term underweight | Bearish (structural barriers to entry declining) |

| Chinese real estate, basic materials, industrials, energy, telecom | Asset-heavy industries | Account for more than one-third of EM portfolio | Bullish (current earnings and valuations do not incentivize new capacity) |

| High-yield financial businesses | Financial companies in consolidating industries | Account for 25% of EM portfolio | Bullish (current earnings and valuations do not incentivize new capacity) |

Asian tech sector price-to-book ratio climbs steadily from about 2.0x in 2016 to approximately 6.5x in 2025

Investment Implications

- What it means for investors: Should significantly underweight AI-themed assets and shift toward asset-heavy, cash-flow-rich industries where current valuations do not incentivize new capacity (e.g., Chinese real estate, basic materials, industrials, energy, telecom, and high-yield financial businesses in consolidating industries)

- Specific direction: Overweight "hard, cold cash flows" over "future jam"—i.e., choose companies that can deliver returns through current dividends and moderate reinvestment, rather than relying on optimistic extrapolation of future earnings and growth rates

- Risk warning: Must endure short-term relative underperformance pain, but this is a necessary price for achieving long-term differentiated positive returns