Super cycle or capital cycle?

Hosking Partners is a London boutique founded in 2013 by Jeremy Hosking, a portfolio manager at Marathon Asset Management for over 25 years. It runs a single global equity strategy built on the capital-cycle, supply-side approach — contrarian, long-term, and unusually diversified (350+ holdings) under a multi-counsellor model, managing around $5.5bn.

In plain words

This report looks at the three big memory-chip makers (Samsung, SK Hynix, Micron), whose stocks have surged 5–8x in the past year to over $1 trillion each. The author argues that while AI is boosting demand for their chips, history shows high profits always attract new supply, crashing prices. These stocks trade at just 6–10 times earnings (meaning the market doubts profits will last), while AI startups like OpenAI get sky-high valuations. The advice: take profits gradually and don't assume 'this time is different.' Worth reading because it explains why these soaring chip stocks may still be risky.

Hosking Partners' report explores whether the global DRAM memory semiconductor industry is in a "super cycle" or a "capital cycle." It focuses on the three dominant players—Micron, SK Hynix, and Samsung Electronics—whose stock prices have risen 5x to 8x over the past 12 months, pushing their market

Theme and Background

This chapter examines whether the global DRAM memory industry is currently in an "AI-driven super cycle" or a "capital cycle theory-dominated supply-constrained cycle." Against the backdrop of Hosking Partners holding shares in Micron, SK Hynix, and Samsung Electronics since 2014, the report analyzes whether these stocks—after rising 5–8x over the past 12 months (with market capitalizations all exceeding $1 trillion)—still have upside potential or are already overvalued. The author seeks to clarify whether demand expansion triggered by the AI boom, or the industry's historical nature of extreme volatility driven by capital expenditure, is the core logic behind current pricing.

Core Thesis

The author's core judgment is: The DRAM industry is currently in a demand-driven "super cycle," but capital cycle theory (supply discipline) remains key to understanding future returns. History shows that high profits inevitably attract new supply, leading to price declines. Although current P/E ratios appear reasonable (6–10x), the author believes the probability of "this time is different" is low and advises cautious profit-taking to reduce positions. Counterintuitively, while the market assigns extremely high valuations to AI labs (e.g., OpenAI, Anthropic) due to the AI frenzy, it maintains low valuations (6–10x P/E) for DRAM companies, indicating that the market does not believe high profits are sustainable—the shadow of historical one-way price plunges still looms.

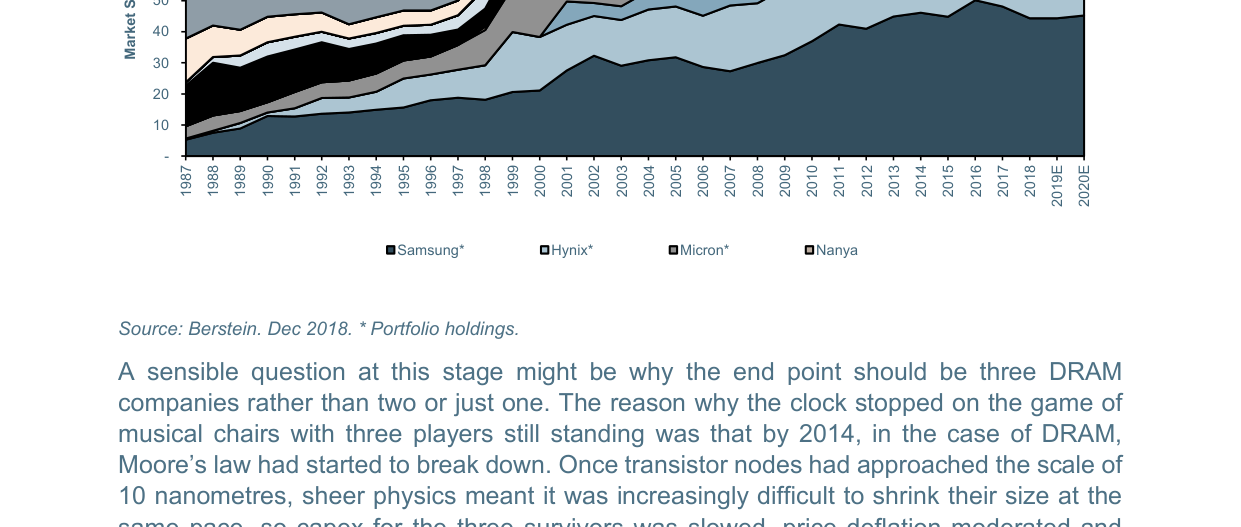

DRAM market share concentrated from over 30 companies in 1987 to just three dominant players by 2020, with Samsung, SK Hynix, and Micron collectively holding 97% market share

Key Arguments and Data

- Historical Price Collapse: From 1974 to 2013, the price of 1MB DRAM fell from $81,920 to $0.007, a decline of 12 million times.

- Industry Consolidation: From Intel's exit from DRAM in 1985 (then stating "the high-volume commodity DRAM market continues to be weak as global overcapacity depresses prices") to 2014, the number of DRAM companies shrank from over 30 to three, with Micron, SK Hynix, and Samsung accounting for 97% of market share.

- Destructive Impact of Moore’s Law: Transistor density doubles every two years, costs drop 50%, but competition causes price declines to outpace cost reductions. Companies are forced to continuously increase capital expenditure to remain competitive, struggling to generate returns.

- Capital Cycle Turning Point: In 2014, Moore’s Law began to slow due to physical limits (10nm node), capital spending decelerated, price declines narrowed, and returns gradually recovered. The three companies' price-to-book ratios fluctuated between less than 1x and 3x, allowing the author to make counter-cyclical additions and reductions.

- AI-Driven Demand Surge: After the launch of ChatGPT in November 2022, demand for high-bandwidth memory (HBM) exploded. HBM consumes four times the wafer capacity of standard DRAM, leading to HBM supply shortages and high prices, while also crowding out standard DRAM capacity, triggering a dual price increase.

- Supply Constraints: Building a new chip fabrication plant takes 12–18 months (shell + cleanroom ~1 year, equipment installation and ramp-up 6 months), and HBM requires an additional 5–6 months from wafer start to output. Chinese competitor CXMT (still lagging in technology) plans an IPO this year to raise funds for capacity expansion.

- Valuation Comparison: The three DRAM giants trade at forward P/E of just 6–10x; in contrast, AI labs (OpenAI, Anthropic, SpaceX) command extremely high IPO valuations, yet the market does not assign a similar premium to DRAM companies, suggesting the market does not believe profits are sustainable.

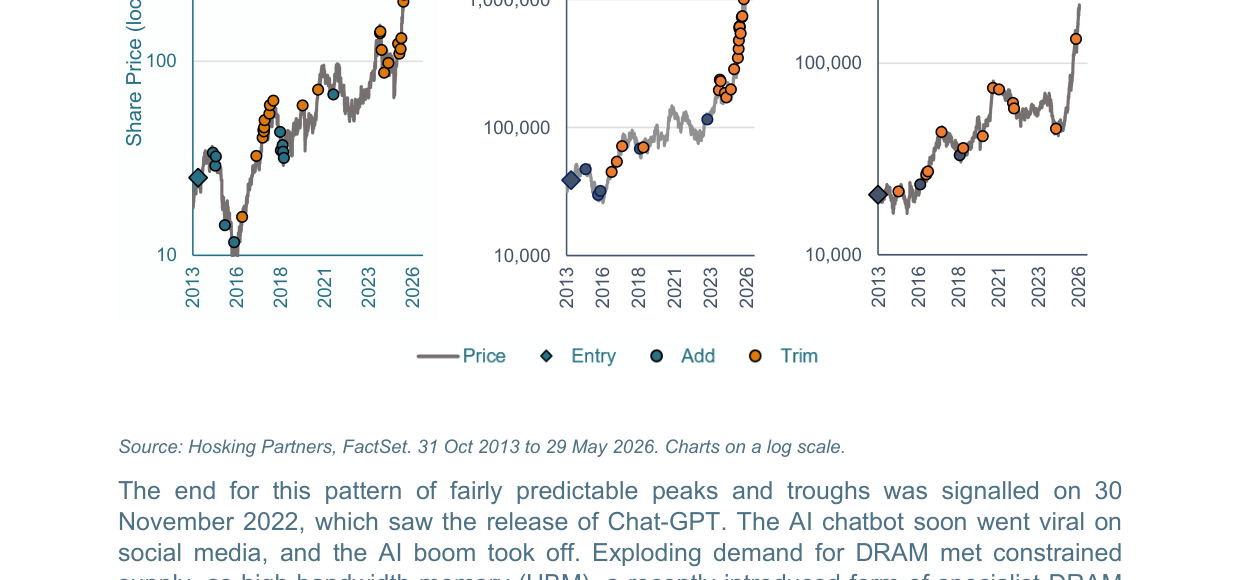

Micron's stock price rose from around $20 in 2013 to nearly $1,000 in 2026 (log scale), with multiple Entry, Add, and Trim operations marked

Companies/Assets Covered

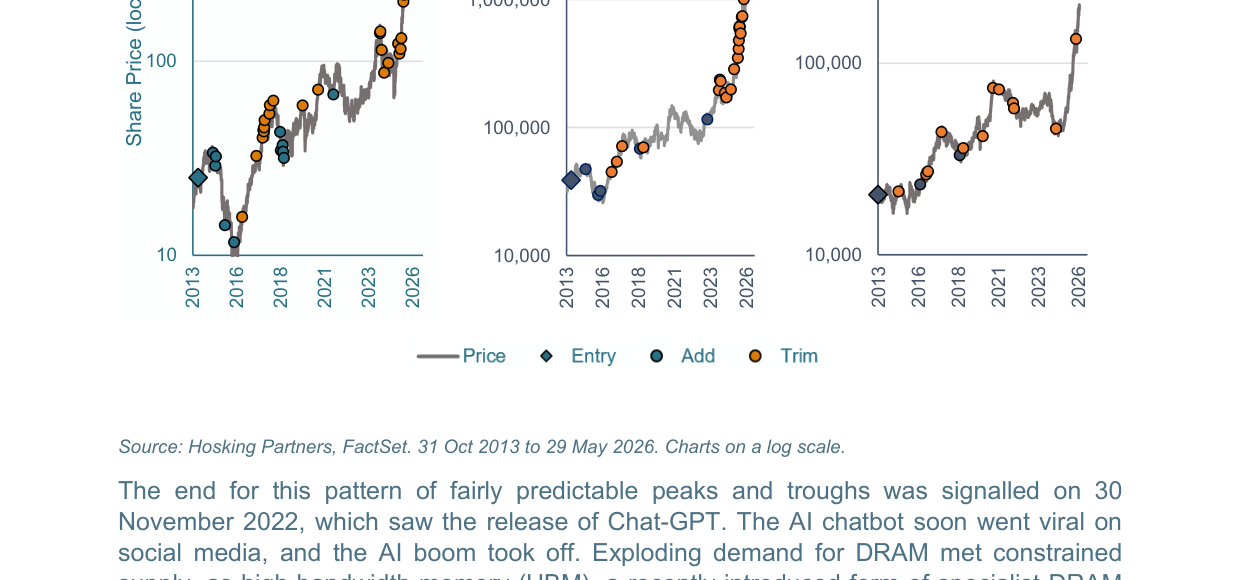

SK Hynix's stock price surged from approximately KRW 30,000 in 2013 to nearly KRW 2,000,000 in 2026, showing a significant long-term upward trend

| Company/Asset | Role | Key Data | Bullish/Bearish |

|---|---|---|---|

| Micron (USA) | One of the Big Three DRAM makers, HBM supplier | Stock price up 5–8x over the past 12 months (recent pullback) | Neutral-cautious; author has partially taken profits |

| SK Hynix (South Korea) | One of the Big Three DRAM makers, key HBM supplier | Fell into loss in 2023 due to DRAM price collapse | Same as Micron, long-term positive but near-term overvalued |

| Samsung Electronics (South Korea) | One of the Big Three DRAM makers | Market cap exceeds $1 trillion | Similar; supply discipline improved but AI demand uncertain |

| CXMT (China) | Potential new competitor | Plans 2026 IPO to fund capacity expansion; technology still lags | Bearish; represents new supply risk |

| OpenAI / Anthropic / SpaceX | AI labs (not investment targets) | Upcoming IPOs; valuations based on "heroic" assumptions (extremely high) | Comparison; market valuations far exceed those of DRAM companies |

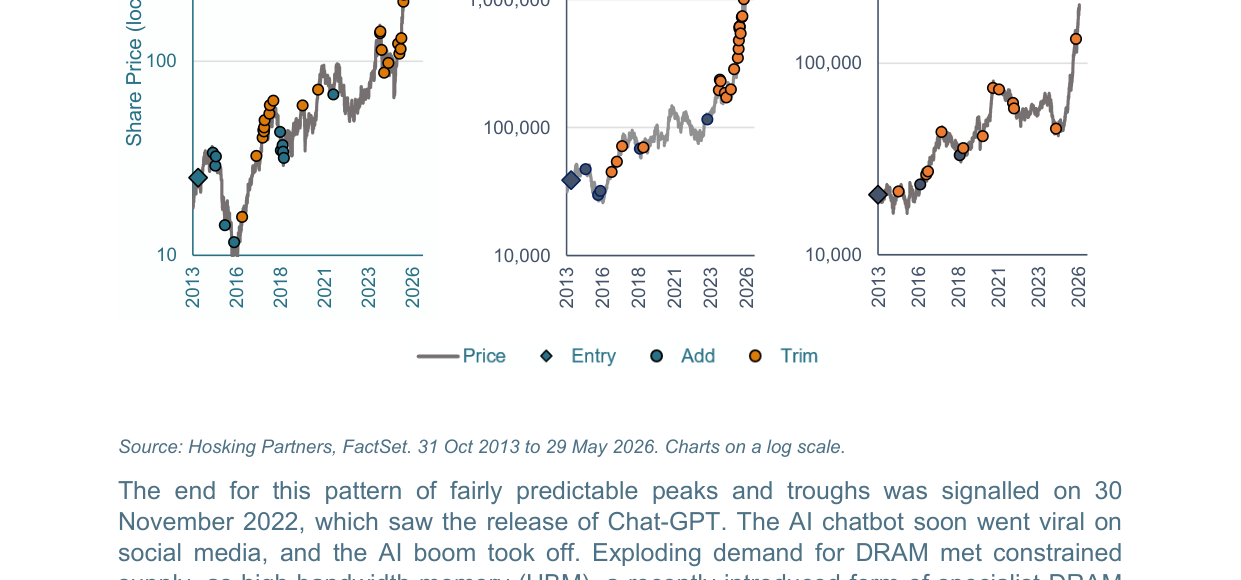

Samsung Electronics' stock price rose from approximately KRW 20,000–30,000 in 2013 to KRW 200,000–300,000 in 2026, experiencing multiple cyclical fluctuations

Investment Implications

- Near-term caution, long-term core holding. The author believes current valuations (6–10x P/E) do not reflect extreme froth in a "super cycle," but high profits inevitably attract new supply (especially from CXMT and existing players expanding capacity), leading to price declines. The recommendation is to gradually take profits on price rallies while maintaining some exposure to benefit from the structural demand for memory chips in the AI arms race.

- Monitor supply-side signals: The enforceability of long-term HBM supply agreements (customer prepayments, committed volumes) remains uncertain; CXMT's IPO and capacity ramp-up represent potential risks. If HBM supply bottlenecks ease or new capacity accelerates, price pressure will intensify.

- Revert to the capital cycle framework: The report emphasizes that even with AI-driven demand, the industry's fundamental nature (persistent high capital expenditure, one-way downward price trend) has not changed. Investors should avoid using "this time is different" as a reason for long-term holding and should reduce positions when price-to-book ratios are elevated (e.g., above 3x).